Overview

On 27 February 2026, Paramount Skydance and Warner Bros. Discovery (WBD) signed a definitive merger agreement valued at approximately $110 billion, a landmark transaction that will see Paramount acquire the entirety of WBD's assets. [1] The deal carries an equity value of $81 billion and is expected to close in the third quarter of 2026, pending regulatory and shareholder approval. [2]

This is more than a simple consolidation play. It is a high-stakes bet on the future of media: a conviction that a fully integrated content and distribution stack is the only viable path forward in a market defined by streaming competition and declining linear viewership. The deal's success or failure will have profound implications for the entire industry, from content creators to consumers, and from advertisers to regulators.

For those of us who work in M&A advisory, the mechanics of this deal are as instructive as the outcome. The bidding war, the financing structure, the regulatory strategy, and the political dimensions all offer a masterclass in how large-scale corporate transactions actually get done.

| Metric | Detail |

|---|---|

| Acquirer | Paramount Skydance (David Ellison, CEO) |

| Target | Warner Bros. Discovery (all assets) |

| Total Transaction Value | ~$110 billion |

| Equity Value | $81 billion |

| Price Per WBD Share | $31.00 cash + $0.25/share ticking fee per quarter after Dec 31, 2026 |

| Debt Financing | $57.5 billion from Bank of America Merrill Lynch, Citi, and Apollo Global Management |

| Equity Financing | $45.7 billion from Larry Ellison; ~$24 billion from Middle Eastern SWFs |

| Combined Debt Load | ~$87 billion (WBD's $33B + Paramount existing + new deal debt) |

| Expected Close | Q3 2026 |

| Shareholder Vote | Early spring 2026 (expected) |

The Bidding War: How Paramount Won

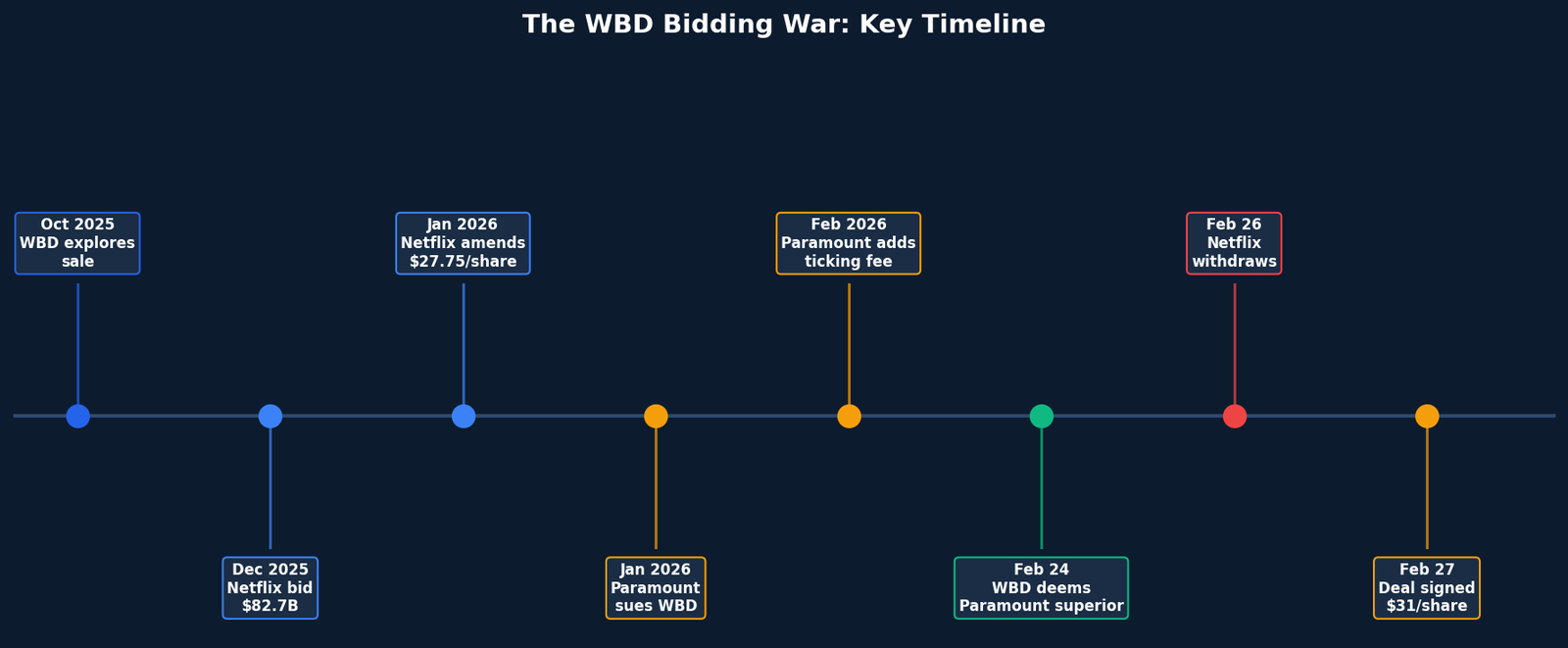

The road to this agreement was a masterclass in high-stakes negotiation and strategic brinkmanship. The story begins in October 2025, when WBD revealed it was exploring a potential sale after receiving unsolicited interest from several major players. [3] What followed was a five-month bidding war that reshaped the competitive dynamics of the entire media industry.

In December 2025, Netflix stunned the industry by announcing an $82.7 billion deal to acquire WBD's film, television, and streaming assets. Critically, Netflix's bid was for the content production capability only, leaving the linear TV networks, including CNN, HGTV, TBS, and TNT, behind. [3] This was a deliberate strategic choice: Netflix wanted the content factory, not the legacy distribution infrastructure.

Paramount, led by David Ellison and backed by his father Larry Ellison, saw a different path. Their thesis was that a full-stack acquisition, combining content creation with distribution across both streaming and linear, was the only way to build a genuinely competitive counterweight to Netflix. Their initial offers were repeatedly rejected by the WBD board, which cited concerns over Paramount's heavy debt load and the complexity of its investor group. [4]

Paramount's eventual success came through a combination of financial engineering and regulatory confidence. They introduced a $0.25 per share ticking fee for each quarter the deal failed to close by year-end, a signal of conviction in their regulatory approval timeline. [5] They agreed to pay the $2.8 billion breakup fee owed to Netflix if WBD terminated their existing agreement. [6] And they raised their final offer to $31.00 per share in cash, a price Netflix ultimately declined to match.

"The transaction we negotiated would have created shareholder value with a clear path to regulatory approval. However, we've always been disciplined, and at the price required to match Paramount Skydance's latest offer, the deal is no longer financially attractive, so we are declining to match the Paramount Skydance bid."

Ted Sarandos and Greg Peters, Netflix Co-CEOs, 26 February 2026 [8]

Netflix's withdrawal was not a defeat. They collected a $2.8 billion termination fee for walking away, a significant return on the time and capital invested in the bidding process. [9] Their statement also reveals something important about their valuation discipline: at $31 per share, the deal was no longer financially attractive. That tells us something about where Netflix sees the intrinsic value of WBD's assets.

Figure 1: The WBD bidding war timeline, from the initial sale announcement in October 2025 to the signed agreement on 27 February 2026.

The Financing: A Mountain of Debt

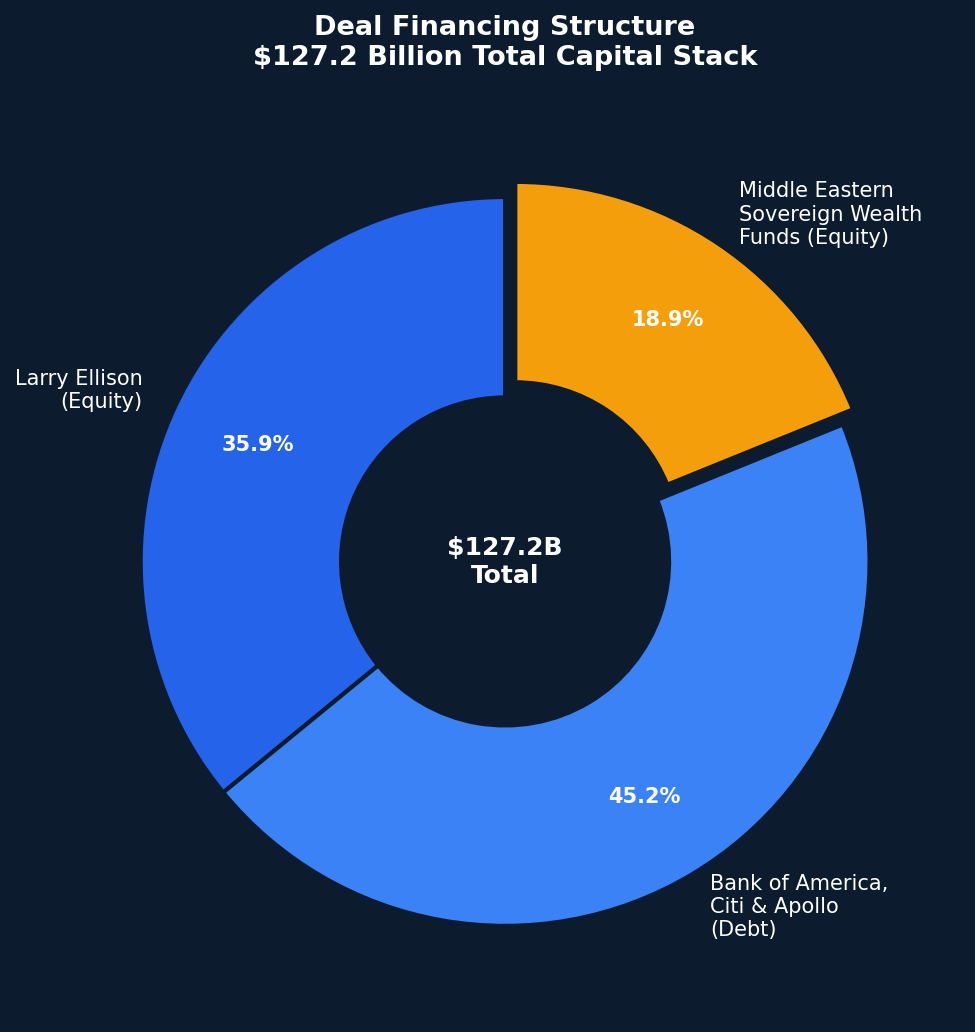

The deal's financing structure is as ambitious as its strategic vision, and it is the element that carries the most significant long-term risk. The acquisition will be funded through a combination of debt and equity that leaves the combined entity carrying approximately $87 billion in total debt. [10]

The debt component, $57.5 billion arranged by Bank of America Merrill Lynch, Citi, and Apollo Global Management, is the largest single component of the financing package. [10] Apollo's involvement is notable: the alternative asset manager is not just providing debt financing but is also a strategic partner with deep media sector expertise and a portfolio of content assets.

The equity side is equally interesting. Larry Ellison's $45.7 billion personal commitment is the cornerstone of the deal, but the involvement of Middle Eastern sovereign wealth funds, approximately $24 billion or 21.6% of the total capital stack, from Saudi Arabia, Qatar, and Abu Dhabi, introduces a geopolitical dimension that regulators will scrutinise carefully. [11]

Figure 2: The deal's capital stack. Total committed capital of approximately $127.2 billion covers the acquisition price plus transaction costs and refinancing of existing WBD debt.

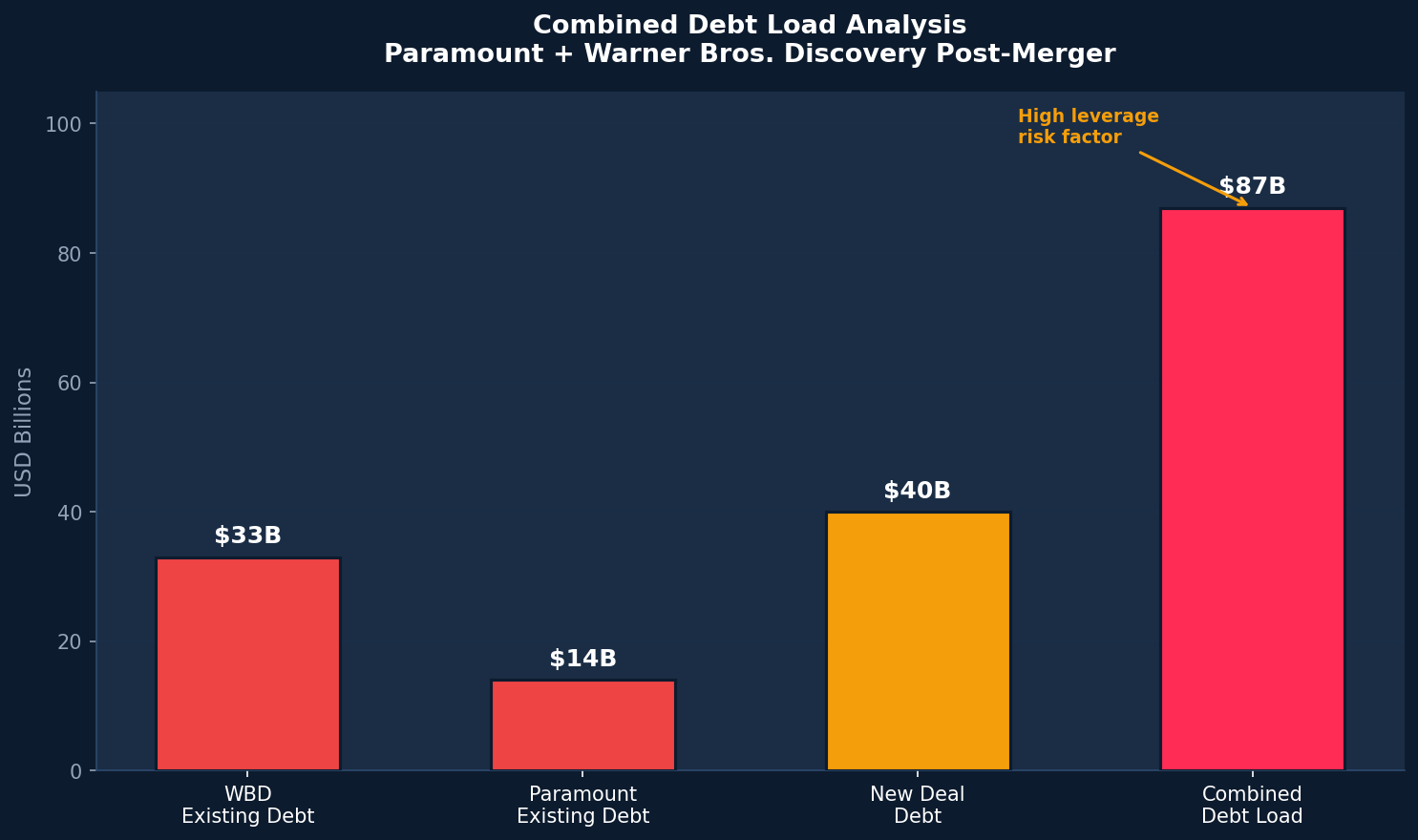

The combined debt load of $87 billion deserves particular attention. WBD itself carries approximately $33 billion in debt, a legacy of the 2022 merger between AT&T's WarnerMedia and Discovery. Paramount brings its own existing debt, and the new deal financing adds a further layer. This level of leverage will require substantial and sustained cost synergies to service, and it significantly reduces the combined company's financial flexibility in the years ahead.

Figure 3: The combined debt load analysis. The $87 billion total represents one of the largest debt burdens ever carried by a media company.

What Paramount Actually Gets

The strategic rationale for the deal becomes clear when you map out exactly what Paramount is acquiring. This is not just a content library acquisition. It is a full-stack media empire spanning production, distribution, streaming, news, and gaming.

| Asset Category | Key Properties |

|---|---|

| Film Studios | Warner Bros. Pictures, New Line Cinema, DC Studios |

| Premium Streaming | HBO Max (combined with Paramount+) |

| Premium Cable | HBO, Cinemax |

| News | CNN (global), combined with CBS News |

| Entertainment Networks | TBS, TNT, TruTV, Adult Swim, Cartoon Network |

| Lifestyle Networks | HGTV, Food Network, Discovery Channel, Animal Planet, Travel Channel |

| Gaming | Warner Bros. Games (Mortal Kombat, Batman: Arkham, Harry Potter IP) |

| IP Libraries | DC Universe, Harry Potter/Wizarding World, Looney Tunes, Game of Thrones |

| International | Eurosport, Max international markets |

The combined Paramount+/HBO Max streaming platform would represent a materially stronger competitor to Netflix. TD Cowen analysts noted in their post-announcement report that the deal presents "a key pro-competitive effect: improved competition in streaming, with Paramount+ and HBO Max representing a materially stronger counterweight to Netflix." [13] This is the argument Paramount will lean on heavily in regulatory proceedings.

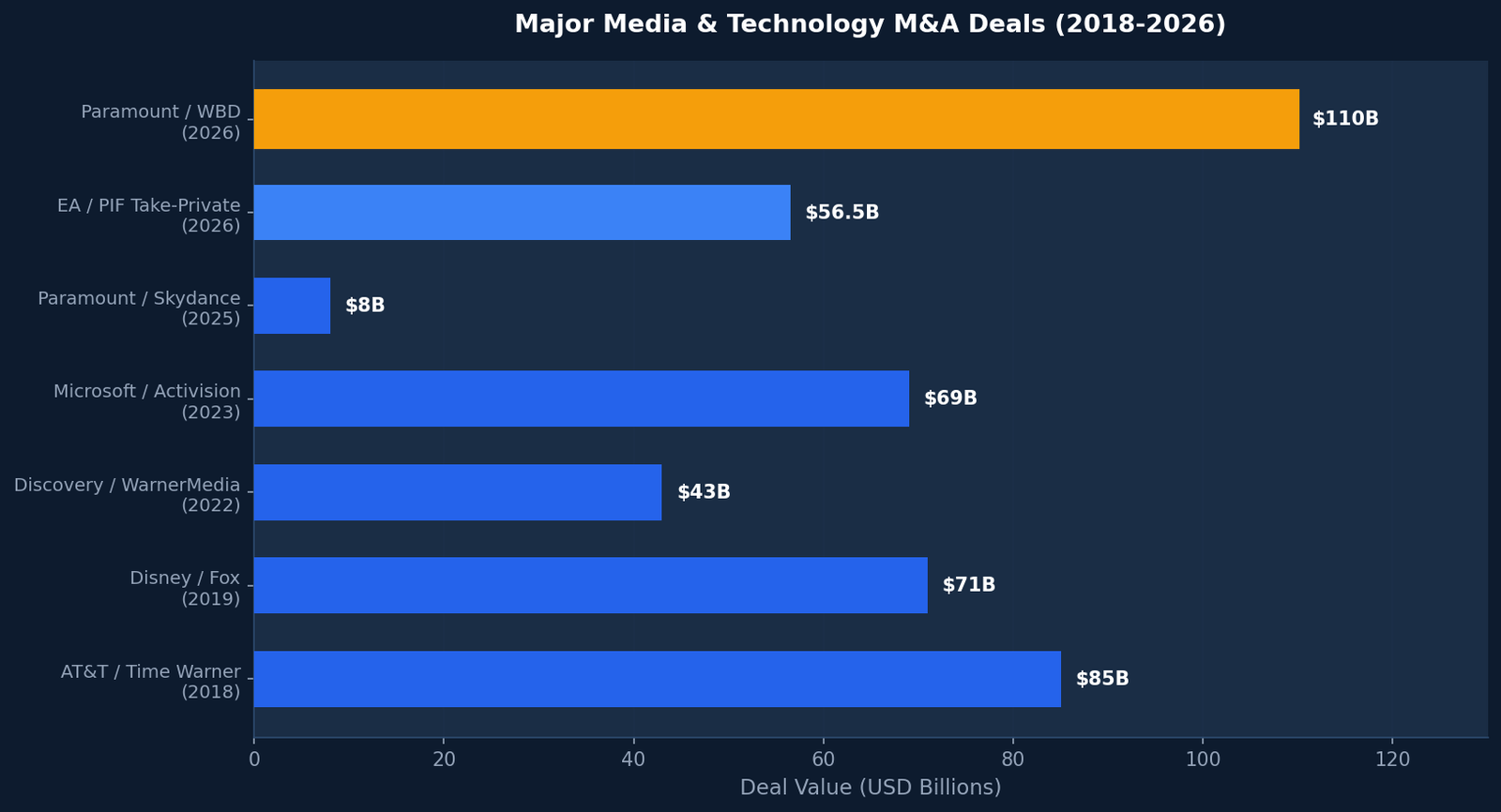

Figure 4: Historical context. The Paramount-WBD deal at $110 billion surpasses the AT&T/Time Warner transaction ($85B, 2018) as the largest media M&A deal in nearly a decade.

The Regulatory Gauntlet

The deal now faces a complex and politically charged regulatory review process. Paramount's legal team has been working this angle aggressively. Their lawyer, Makan Delrahim, filed with the DOJ for approval in December 2025, before Paramount even had a signed deal, a deliberate signal of regulatory confidence. [4] The initial DOJ antitrust deadline passed without comment from Trump administration regulators, which analysts read as a positive indicator. [13]

However, the regulatory landscape is far from clear. Here are the key risk factors:

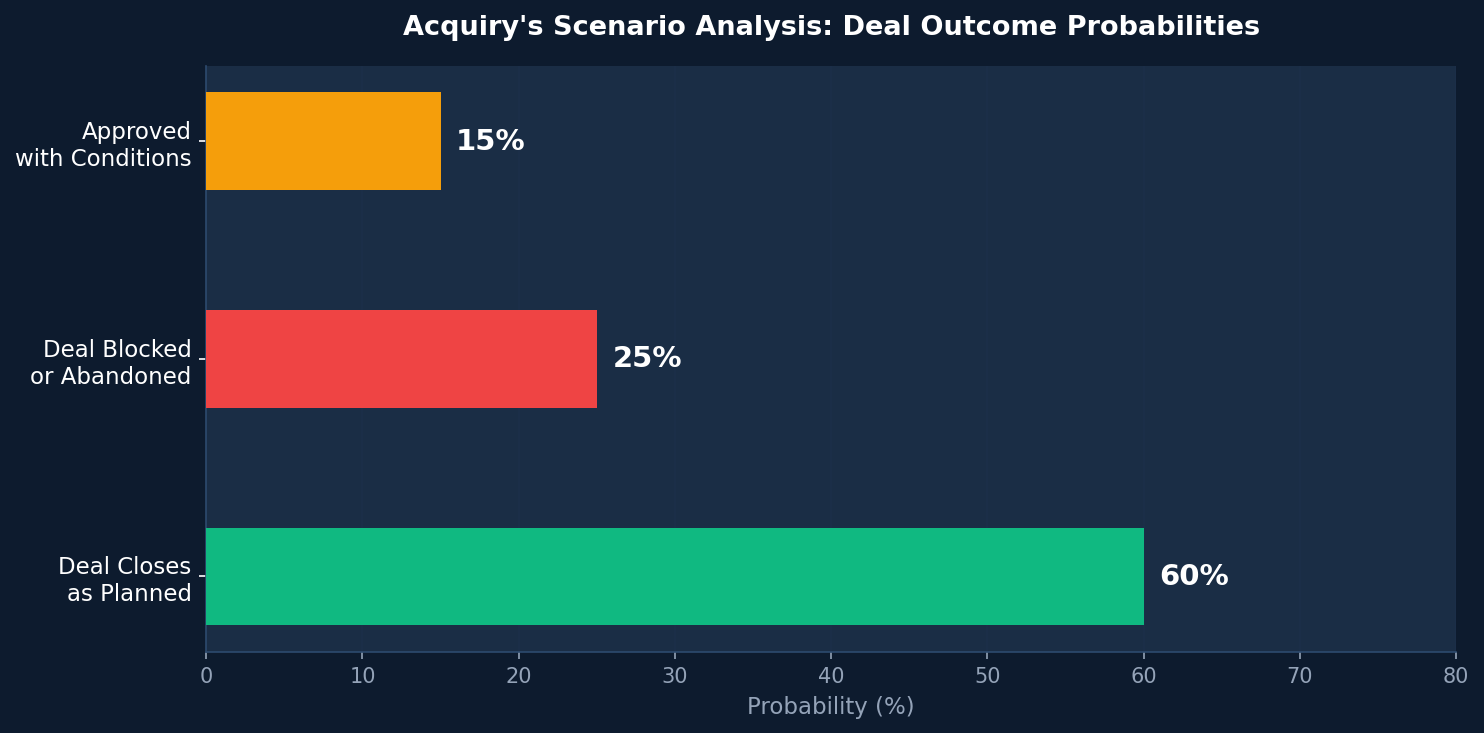

Acquiry's View: The Scenarios Ahead

From an M&A transaction perspective, we assess three primary scenarios for how this deal could unfold. These are not predictions; they are structured probability assessments based on the regulatory environment, the political dynamics, and the financial fundamentals.

Figure 5: Acquiry's scenario probability assessment. The 60% base case assumes regulatory approval without material conditions, consistent with the Trump administration's broadly deal-friendly posture.

Implications for the Broader Media M&A Market

Regardless of how this specific deal resolves, it has already changed the landscape for media M&A in several important ways.

First, it has established a new valuation floor for premium content assets. Netflix's willingness to bid $82.7 billion for studios and streaming alone, and Paramount's willingness to pay $110 billion for the full stack, sets a reference point for any future transaction involving comparable assets. Comcast, Disney, and Apple are all watching this process carefully.

Second, the deal demonstrates that sovereign wealth fund capital is now a primary driver of mega-deal financing in media and technology. The Middle Eastern SWFs backing this deal are the same capital pools that funded the EA take-private ($55 billion) and a wave of gaming and digital infrastructure acquisitions. This is structural, not cyclical.

Third, the Netflix exit is instructive. A $2.8 billion termination fee for walking away from a deal that was "no longer financially attractive" tells you something important about Netflix's capital allocation discipline. They were willing to pay up to approximately $27.75 per share for WBD's content assets. Above that price, the return on capital did not justify the risk. That is a useful data point for anyone trying to value media content businesses.

For Acquiry's clients operating in the media and content M&A space, the key takeaway is that the market for premium content assets has bifurcated sharply. Assets with strong IP, recurring audience relationships, and multi-platform distribution capability are commanding significant premiums. Assets without those characteristics are being repriced downward as the cost of capital rises and the streaming wars enter a consolidation phase.

Conclusion

The Paramount-WBD merger is a defining moment for the media industry. It is a bold, high-risk, high-reward bet on the future of content and distribution. The deal's success will depend not only on navigating a complex and politically charged regulatory landscape, but also on the ability of the combined company to manage its massive debt load and realise the promised synergies in a market that is still in structural transition.

From an M&A transaction perspective, the deal's most important lesson is about process. Paramount won not because they had the best initial offer, but because they had the clearest regulatory strategy, the most credible financing commitment, and the willingness to keep raising their bid when the WBD board kept saying no. That persistence, backed by a coherent strategic thesis, is what separates successful acquirers from unsuccessful ones.

We will continue to monitor this transaction as it moves through regulatory review. If you are operating in the media, content, or digital asset space and want to understand what this deal means for your own M&A strategy, we are available for a direct conversation.