Overview

On November 19, 2025, Adobe (Nasdaq: ADBE) and Semrush Holdings (NYSE: SEMR) announced a definitive agreement under which Adobe will acquire Semrush in an all-cash transaction at $12.00 per share, representing a total equity value of approximately $1.9 billion. The deal was unanimously approved by both boards on announcement day, with Semrush's founders and major stockholders representing over 75% of voting power committing to vote in favour. Shareholders formally approved the merger at a special meeting on February 3, 2026. Closing is targeted for the first half of 2026, subject to remaining regulatory clearances.

The acquisition price represents a 74% premium to Semrush's closing price of $6.89 the day before the announcement. At 4.3x trailing revenue and 4.2x ARR, the deal sits at the lower end of the SaaS acquisition multiple range, a reflection of Semrush's modest profitability profile rather than any weakness in the strategic thesis. Adobe, a $21.5 billion revenue company, is paying roughly 9% of its annual revenue to acquire a platform that it believes will become a foundational layer in the next generation of AI-driven marketing infrastructure.

Acquiry Assessment: This is a strategically coherent deal at a fair price. Adobe is not overpaying. At 4.3x revenue with 18% growth and 12% FCF margin, Semrush was trading at a discount to SaaS peers before the announcement. The 74% premium corrects that undervaluation while still leaving Adobe with a defensible entry point. The real question is integration execution, not deal economics.

What Is Semrush

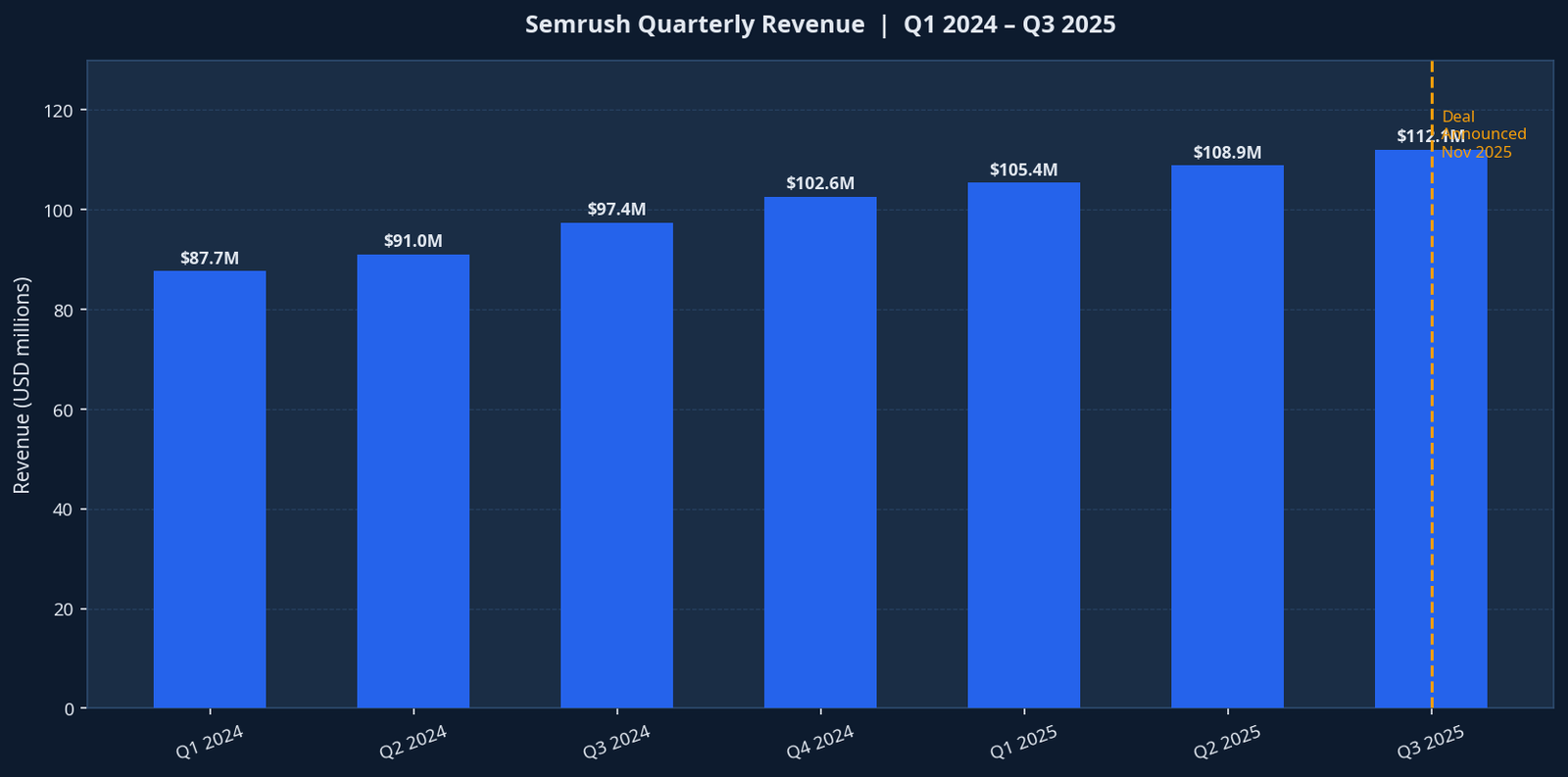

Founded in 2008 and headquartered in Boston, Semrush is a 17-year-old SaaS platform that began as an SEO keyword research tool and evolved into a comprehensive brand visibility and competitive intelligence suite. As of Q3 2025, the company reported ARR of $455.4 million, quarterly revenue of $112.1 million (up 15% year-over-year), and approximately 117,000 paying customers across 143 countries.

Semrush's product portfolio spans six core capability areas: SEO analytics, competitive research, content marketing, advertising intelligence, social media management, and the newer AI-native GEO (Generative Engine Optimization) tracking tools. The company's flagship product at the time of the acquisition was Semrush One, launched in October 2025, which consolidates traditional search metrics with real-time visibility tracking across AI platforms including ChatGPT, Google Gemini, Perplexity, and Claude.

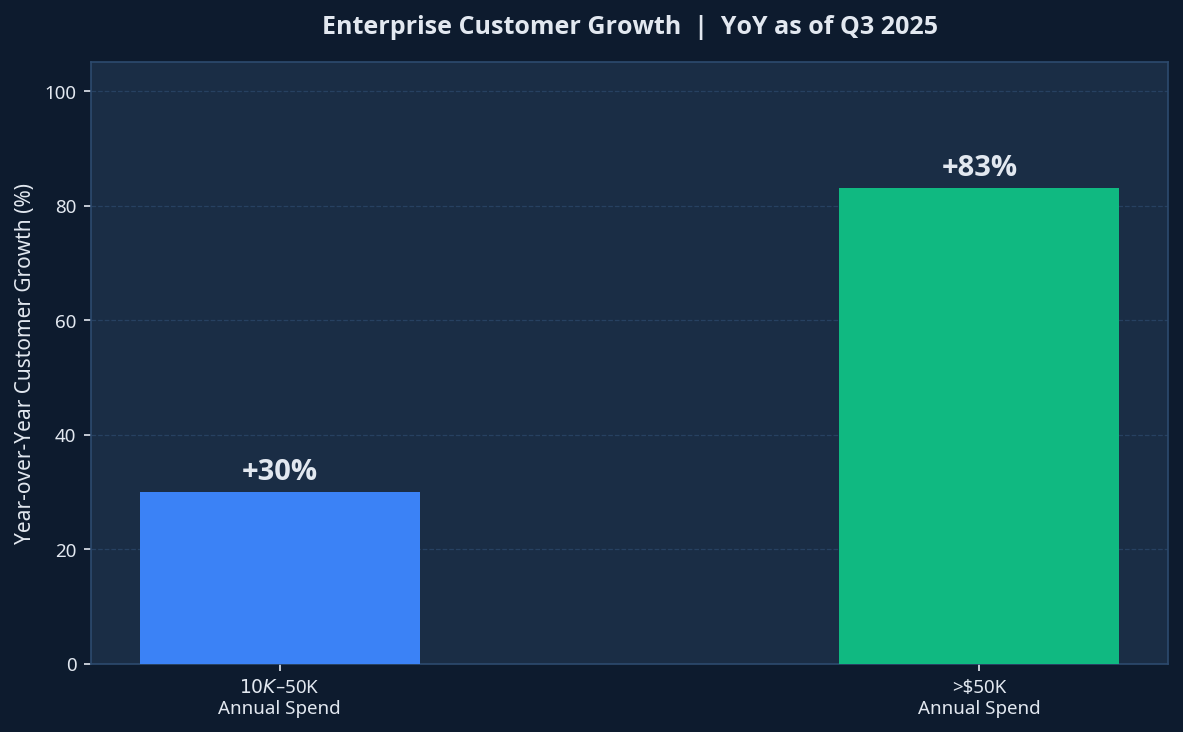

The enterprise segment has been the primary growth driver. Customers paying more than $50,000 annually grew 83% year-over-year as of Q3 2025, and the enterprise cohort's ARR grew 33% year-over-year in the same period. Key enterprise customers include Amazon, TikTok, UPS, Publicis Groupe, Wix, and JPMorganChase. This upmarket trajectory is directly aligned with Adobe's existing customer base, which includes 99% of the Fortune 100.

Semrush quarterly revenue, Q1 2024 through Q3 2025. Revenue grew from $87.7M to $112.1M over seven quarters, with the deal announced immediately after Q3 2025 results.

Deal Structure and Terms

The transaction is structured as a straightforward all-cash acquisition. Adobe will acquire 100% of Semrush's outstanding shares at $12.00 per share. There are no contingent consideration components, earnouts, or equity rollovers disclosed in the definitive agreement. The clean structure reflects Adobe's preference for certainty and its capacity to fund the acquisition from existing cash and credit facilities without requiring equity issuance.

| Deal Parameter | Detail |

|---|---|

| Announced | November 19, 2025 |

| Structure | All-cash acquisition, 100% of shares |

| Price per share | $12.00 |

| Total equity value | ~$1.9 billion |

| Premium to pre-announcement close | +74% (vs $6.89 close) |

| Revenue multiple | 4.3x trailing revenue (~$444M FY2025 guidance) |

| ARR multiple | 4.2x ($455.4M ARR as of Q3 2025) |

| Shareholder vote | Approved February 3, 2026 (special meeting) |

| Founder/major stockholder support | Over 75% of voting power committed pre-announcement |

| Expected close | First half of 2026 |

| Adobe financial advisor | None disclosed |

| Adobe legal advisor | Wachtell, Lipton, Rosen & Katz |

| Semrush financial advisor | Centerview Partners LLC |

| Semrush legal advisor | Davis Polk & Wardwell |

Three Semrush stockholders filed lawsuits in New York and Massachusetts courts between January 13 and 15, 2026, alleging proxy statement deficiencies. These are routine merger objection suits and are not expected to block or materially delay the transaction. The shareholder vote proceeded on schedule and passed with the required majority on February 3, 2026.

Strategic Rationale: The GEO Thesis

Adobe's stated rationale centres on what it calls the "agentic AI era" of marketing, in which generative AI platforms are becoming the primary interface between consumers and brands. The traditional search funnel, where a user types a query into Google and clicks through to a website, is being disrupted by AI-generated answers that synthesise information from multiple sources without requiring a click. Adobe Analytics data cited in the press release showed that traffic from generative AI sources to US retail sites increased 1,200% year-over-year in October 2025.

This shift creates an entirely new problem for marketers: how do you ensure your brand appears favourably in an AI-generated answer? The discipline emerging to address this is Generative Engine Optimization (GEO), and Semrush's Semrush One platform is one of the earliest enterprise-grade tools capable of tracking brand visibility across AI models in real time. For Adobe, which already sells Adobe Analytics, Adobe Experience Manager, and Marketo to the same enterprise marketing teams, Semrush fills a critical gap in the data stack.

"Brand visibility is being reshaped by generative AI, and brands that don't embrace this new opportunity risk losing relevance and revenue. With Semrush, we're unlocking GEO for marketers as a new growth channel alongside their SEO, driving more visibility, customer engagement and conversions across the ecosystem."

Anil Chakravarthy, President of Adobe's Digital Experience Business

The acquisition also addresses a structural weakness in Adobe's analytics portfolio. Adobe Analytics is strong on owned-channel measurement (website behaviour, campaign attribution, conversion tracking) but has limited capability in competitive intelligence and earned/organic channel visibility. Semrush's competitive research tools, which track competitor keyword rankings, ad spend, content performance, and now AI search presence, give Adobe a dataset it cannot easily replicate internally.

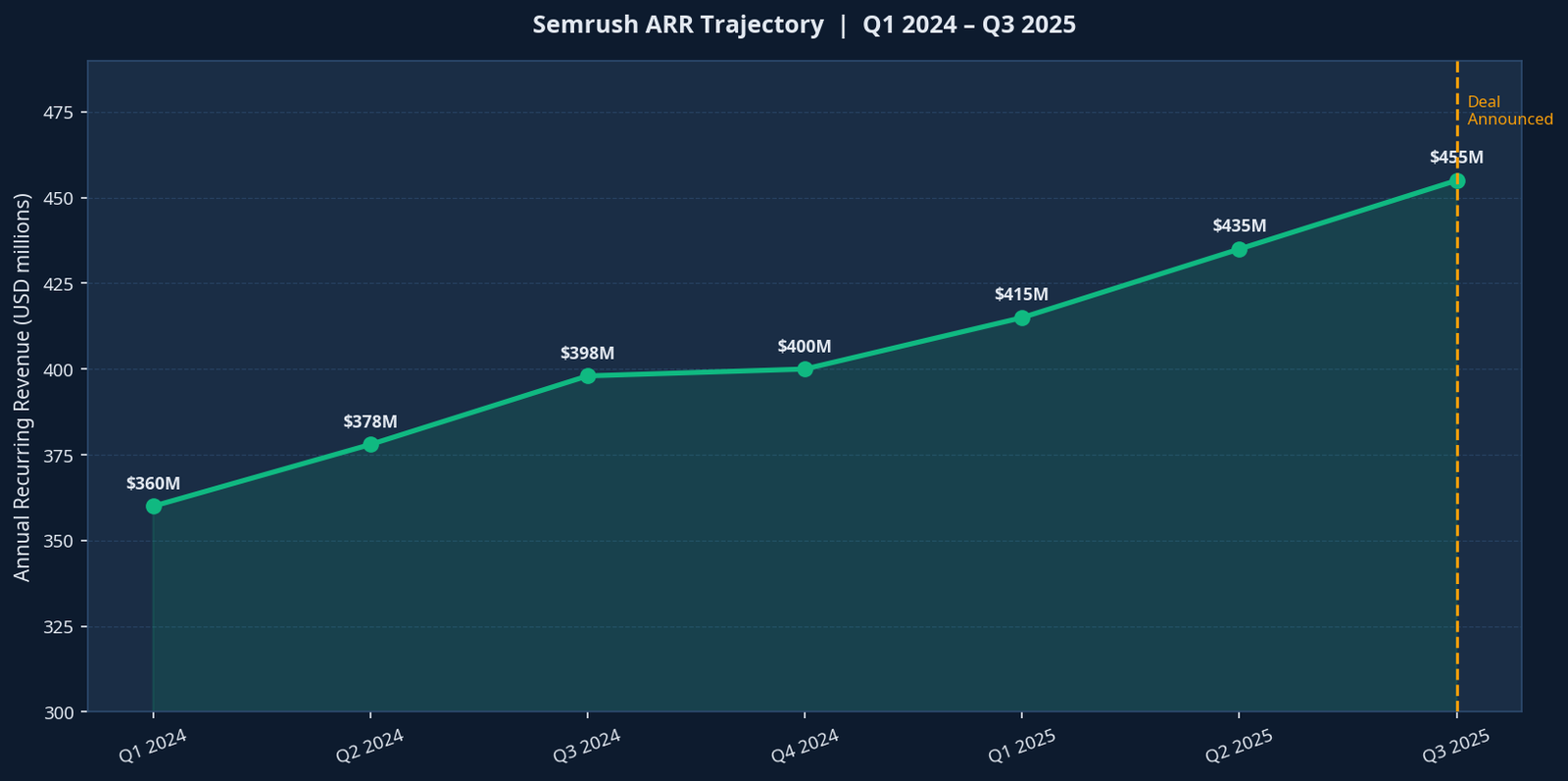

Semrush ARR grew from $360M in Q1 2024 to $455.4M by Q3 2025, a 26% increase over six quarters. Enterprise segment ARR grew 33% year-over-year in Q3 2025.

Adobe's Strategic Context: Post-Figma

Adobe's M&A history is essential context for evaluating this deal. In September 2022, Adobe announced the acquisition of Figma for $20 billion, the largest software acquisition in history at the time. The deal was terminated in December 2023 after the UK's Competition and Markets Authority and the European Commission both raised serious concerns about competitive harm in the design software market. Adobe paid Figma a $1 billion termination fee.

The Figma collapse left Adobe in an awkward position: it had signalled a major strategic pivot toward collaborative design tools, spent three years in regulatory limbo, paid a $1 billion penalty, and emerged with nothing to show for it. The Semrush deal, at $1.9 billion, is a very different transaction. It is smaller, strategically adjacent rather than competitively threatening, and faces minimal antitrust risk given that Semrush does not compete directly with any Adobe product. The HSR filing is a formality rather than a genuine regulatory hurdle.

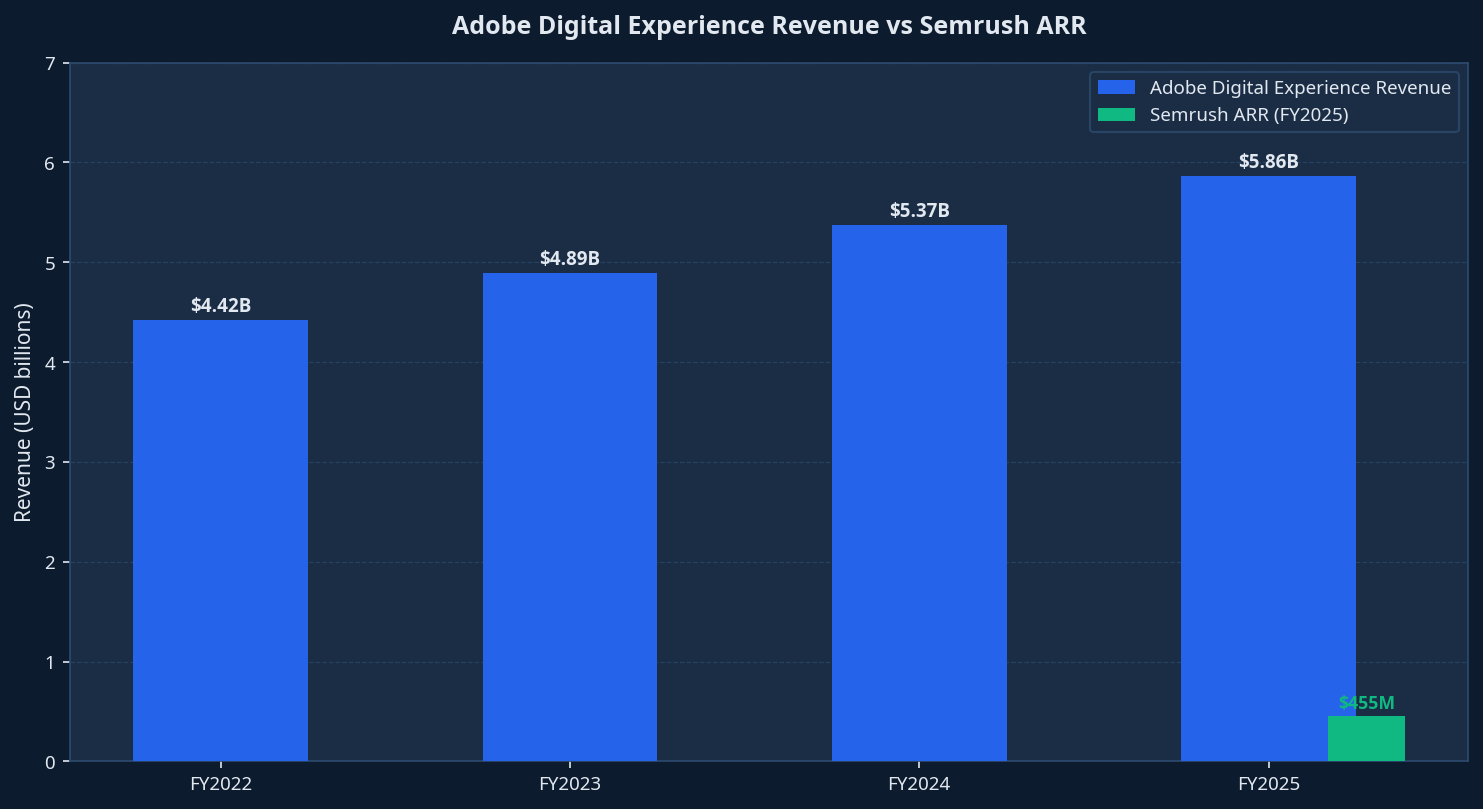

Adobe's Digital Experience segment, which houses the products most relevant to the Semrush integration (AEM, Adobe Analytics, Marketo, Adobe Experience Platform), generated $5.86 billion in revenue in FY2025, up 9% year-over-year. The segment is growing but faces intensifying competition from Salesforce, HubSpot, and a wave of AI-native marketing platforms. Adding Semrush's data and GEO capabilities strengthens the differentiation argument for Adobe's enterprise marketing stack at a critical moment.

Adobe's Digital Experience segment generated $5.86B in FY2025. Semrush's $455M ARR represents approximately 8% of that segment's revenue, a meaningful but digestible addition.

Valuation Analysis

The $1.9 billion deal price implies a 4.3x trailing revenue multiple and a 4.2x ARR multiple. In the context of the broader SaaS acquisition market, this is a conservative valuation for a platform growing at 18% with 12% free cash flow margins. Comparable public SaaS companies in the marketing technology space traded at 6x to 12x revenue in 2024 and 2025. HubSpot, the closest public comparable, traded at approximately 8x revenue through 2024.

The discount to peers reflects several factors. Semrush's GAAP profitability has been inconsistent, with Q3 2025 showing a loss from operations of $4.5 million despite strong non-GAAP margins. The company's customer base, while large at 117,000 paying accounts, skews toward SMB and mid-market, with enterprise penetration still in early stages. The stock had also underperformed the broader SaaS index through 2025, trading below its 2021 IPO price for extended periods, which suppressed the pre-announcement baseline.

Left: The $12.00 deal price represents a 74% premium to Semrush's pre-announcement close of $6.89. Right: At 4.3x revenue, the deal is priced below comparable SaaS acquisitions.

| Metric | Value | Assessment |

|---|---|---|

| Deal price | $12.00/share | Fair |

| Premium to close | +74% | Elevated but justified |

| EV / Revenue (trailing) | 4.3x | Below SaaS peer average |

| EV / ARR | 4.2x | Conservative for 18% growth |

| Revenue growth (FY2025 guidance) | ~18% YoY | Strong |

| Non-GAAP operating margin | ~12% | Modest but improving |

| FCF margin | ~12% | Positive and consistent |

| GAAP operating income (Q3 2025) | -$4.5M | Still loss-making on GAAP basis |

From Adobe's perspective, the deal is financially immaterial in the short term. At $1.9 billion against Adobe's $21.5 billion revenue base and substantial cash position, this is a strategic investment rather than a transformative financial event. The question is whether Semrush's data and GEO capabilities can accelerate Adobe's Digital Experience segment growth rate, which has been decelerating from 11% in FY2024 to 9% in FY2025.

Enterprise Momentum: The Real Asset

The most compelling aspect of Semrush's business at the time of acquisition is not its total ARR but the acceleration in its enterprise segment. The cohort of customers paying more than $50,000 annually grew 83% year-over-year in Q3 2025. The cohort paying more than $10,000 annually grew 30%. This upmarket migration is precisely what Adobe needs: enterprise marketing teams that already use Adobe Analytics and AEM are natural buyers for Semrush's competitive intelligence and GEO tools.

Enterprise customer growth by annual spend tier as of Q3 2025. The high-value segment (over $50K annually) grew 83% year-over-year, signalling strong upmarket traction.

The ARR per paying customer metric also tells an important story. At $3,522 per customer as of FY2024 (up from $3,125 in FY2023), Semrush has been successfully expanding wallet share through upsell. Within an Adobe enterprise account, where the total contract value is often in the hundreds of thousands of dollars, Semrush's tools could command significantly higher pricing as an integrated module rather than a standalone subscription.

Competitive Implications

The Adobe-Semrush combination creates a new competitive dynamic in the marketing technology stack. The most directly affected parties are Salesforce, which acquired Moz (a competing SEO platform) in 2023, and the pure-play SEO tool vendors including Ahrefs and Moz itself. Adobe now has a more comprehensive competitive intelligence and search visibility offering than any of its primary enterprise marketing cloud competitors.

HubSpot, which has been aggressively expanding its enterprise footprint, does not have a comparable SEO or GEO data asset. This acquisition widens the capability gap between Adobe and HubSpot at the enterprise tier. For mid-market buyers who are evaluating marketing platforms, the integrated Adobe-Semrush stack offers a compelling argument for consolidating spend.

The irony of the deal is not lost on market observers: Semrush's data is largely derived from tracking Google search results, and that data now sits inside Adobe's stack, which competes with Google's own marketing tools (Google Analytics, Google Ads, Google Marketing Platform). As AI search erodes Google's dominance, Adobe is positioning itself to benefit from the disruption rather than be exposed to it.

Risk Flag: Semrush's data moat depends on continued access to search engine data and AI platform APIs. If Google, OpenAI, or other AI providers restrict third-party visibility tracking, the core GEO value proposition could be impaired. This is a platform dependency risk that Adobe will need to manage through direct data partnerships post-close.

Integration Pathway

Adobe has not disclosed specific integration plans, which is standard for deals pending regulatory clearance. However, the logical integration pathway is clear from the product architecture. Semrush's data layer connects naturally to Adobe Analytics (competitive benchmarking), Adobe Experience Manager (content optimisation for SEO and GEO), Marketo (campaign performance against organic search), and the newly launched Adobe Brand Concierge (AI-powered brand visibility in conversational interfaces).

The near-term priority will likely be a data connector between Semrush One and Adobe Analytics, allowing enterprise customers to view owned-channel performance alongside competitive and AI search visibility in a single dashboard. This is a relatively straightforward technical integration and could be delivered within 12 months of close.

The longer-term integration challenge is organisational. Semrush has approximately 3,000 employees and a distinct product culture built around rapid iteration and SEO-native workflows. Adobe's enterprise software culture is more deliberate and compliance-focused. Retaining Semrush's product and engineering leadership through the integration will be critical to preserving the innovation velocity that made the platform valuable in the first place.

Scenario Analysis

GEO Becomes the New SEO

AI search captures 30%+ of query volume by 2027. Semrush One becomes the de facto enterprise standard for GEO tracking. Adobe bundles it into the Digital Experience suite, driving 15%+ ARR growth and accelerating the segment's revenue growth rate back above 12%.

Solid Strategic Add-On

Semrush integrates cleanly into Adobe Analytics and AEM. Enterprise cross-sell adds $150-200M in incremental ARR over three years. GEO adoption grows steadily but does not become a dominant budget line. Deal generates modest but positive financial returns.

Integration Drag

Key Semrush product leadership departs post-close. Integration complexity slows Adobe's Digital Experience roadmap. AI platform data restrictions limit GEO tracking capability. Semrush ARR growth decelerates to single digits as the standalone brand loses momentum inside Adobe's enterprise sales motion.

Key Risks

| Risk | Severity | Mitigation |

|---|---|---|

| AI platform data access restrictions (Google, OpenAI API changes) | High | Direct data partnership negotiations; diversification across AI platforms |

| Key talent retention post-close | Medium | Retention packages; cultural integration planning |

| Integration complexity slowing Digital Experience roadmap | Medium | Phased integration; maintain Semrush as semi-autonomous unit initially |

| GEO market development slower than expected | Medium | Semrush's core SEO business remains strong regardless of GEO timing |

| Regulatory delay (HSR antitrust) | Low | No direct competitive overlap; routine filing expected |

| Shareholder litigation (3 suits filed Jan 2026) | Low | Routine proxy suits; vote proceeded on schedule and passed |

Acquiry View

This deal is well-structured and strategically sound. Adobe is buying a profitable, growing SaaS platform at a below-market multiple, with a clear integration thesis and a genuine product gap to fill. The 74% premium looks large in isolation but is entirely justified given Semrush's pre-announcement undervaluation relative to its growth profile and the strategic value Adobe places on the GEO capability.

The more interesting question is what this signals for the broader marketing technology M&A market. Adobe's move will accelerate consolidation pressure on standalone SEO and digital analytics vendors. Ahrefs, Moz, Conductor, and BrightEdge are now all potential acquisition targets for enterprise software platforms looking to close the same gap Adobe just addressed. HubSpot, Salesforce, and SAP are the most likely acquirers in that second wave.

For founders and investors in the SEO, competitive intelligence, and AI search visibility space: the Adobe-Semrush deal has set a public comparable. A growing, profitable platform in this category with enterprise traction should be able to command 4x to 6x ARR in a strategic sale. The GEO narrative adds a meaningful premium to what would otherwise be a mature SEO tool story.

Bottom Line: Adobe pays a fair price for a strategically essential asset. The deal closes the GEO gap in Adobe's Digital Experience stack at a moment when that gap was becoming a competitive liability. Execution risk is real but manageable. This is the right deal at the right time for Adobe, and it sets a clear market signal for the next wave of marketing technology consolidation.