Deal Overview

On 13 October 2025, Allwyn International AG and OPAP S.A. jointly announced a business combination that will create the world's second-largest listed lottery and gaming operator. The transaction values the combined entity at €16 billion in equity and is structured as an all-share deal, with Allwyn contributing its non-OPAP assets to a new Luxembourg holding company (LuxCo) in exchange for newly issued shares.

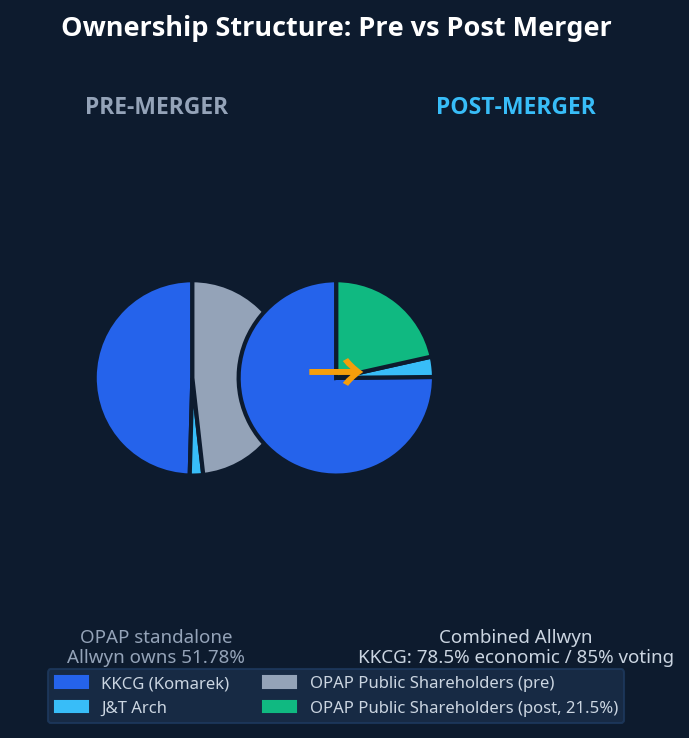

The mechanics are unusual. Allwyn already owns 51.78% of OPAP, so this is not a conventional acquisition of an independent target. It is a consolidation of a controlling stake into full ownership, combined with a public market listing for Allwyn itself. Allwyn has never been publicly traded. By merging into OPAP's listed vehicle and re-domiciling to Switzerland, Allwyn gains access to equity capital markets while OPAP's minority shareholders receive a stake in a materially larger, more diversified business.

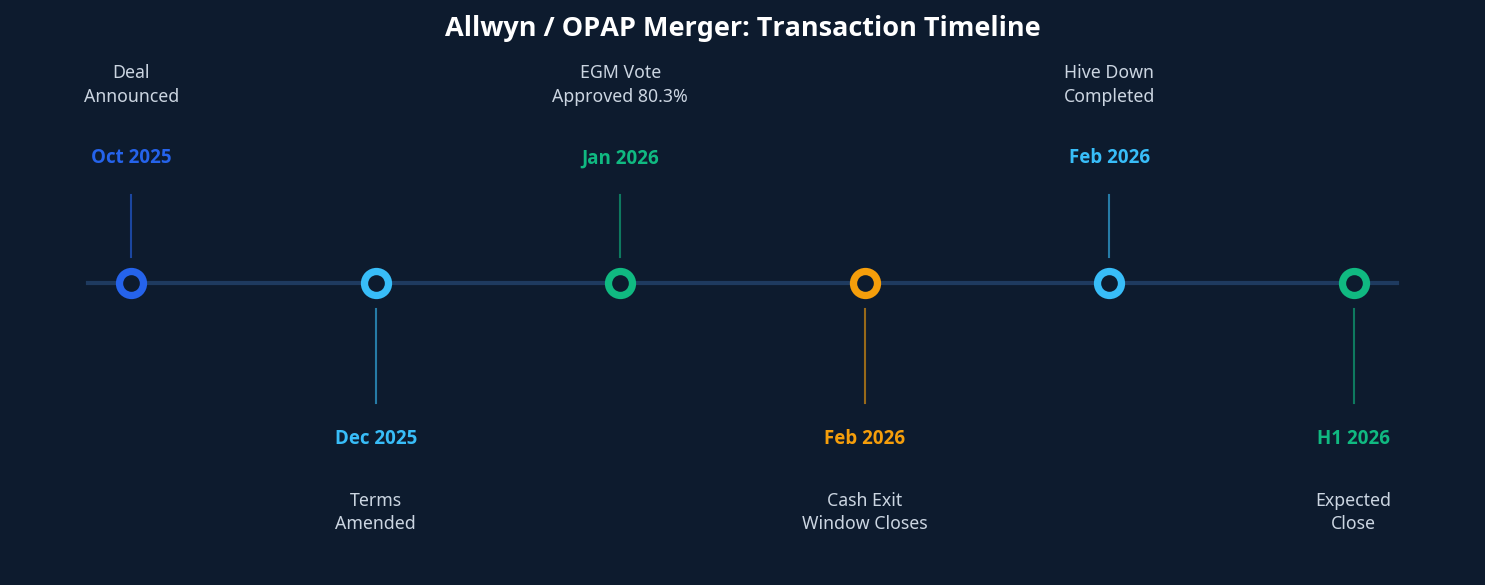

Transaction timeline from announcement (October 2025) through EGM approval (January 2026) to expected close in H1 2026. The hive-down of OPAP's Greek operations was completed in February 2026.

| Parameter | Detail |

|---|---|

| Announcement Date | 13 October 2025 |

| Combined Equity Value | €16 billion |

| Transaction Type | All-share business combination |

| Allwyn's Pre-Deal Stake in OPAP | 51.78% |

| Allwyn Post-Deal Economic Interest | ~78.5% |

| KKCG Post-Deal Voting Control | ~85.0% |

| OPAP Minority Shareholders Post-Deal | ~21.5% economic interest |

| Allwyn Asset Contribution Value | €8,967 million (net of liabilities) |

| Consideration: Ordinary Shares | €8,806M (437.7M shares at €20.12/share) |

| Consideration: Preferred Shares | €161M (536.2M shares, 5% fixed coupon) |

| EGM Vote | 7 January 2026 — approved 80.3% |

| Cash Exit Window Closed | 9 February 2026 (limited take-up) |

| Hive-Down Completed | February 2026 |

| Expected Close | H1 2026 |

| Listing Post-Close | Athens Stock Exchange (primary); London or NYSE (planned) |

| Advisors | Morgan Stanley (OPAP fairness opinion), Grant Thornton (related party) |

Who Is Allwyn

Allwyn is a privately held multi-national gaming company controlled by Czech billionaire Karel Komarek through his KKCG investment group. Founded in 2012 and headquartered in Lucerne, Switzerland, Allwyn operates national lottery and gaming concessions across Europe and North America. Its portfolio includes the UK National Lottery (won in 2022, launched 2024), the Czech Republic's national lottery, Austria's WINWIN, Italy's Sisal, and US operations in Illinois and Georgia.

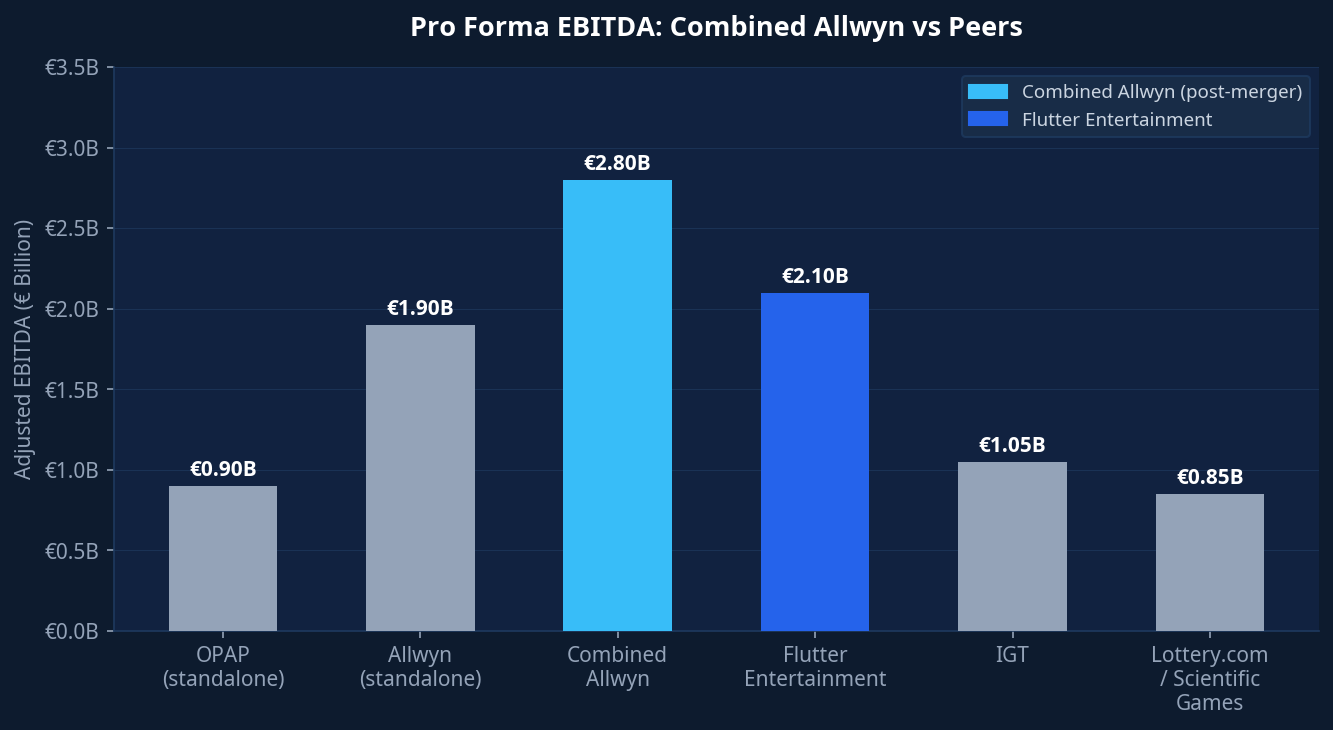

Allwyn's financial profile is substantial. In Q1 2025, the company reported total revenue of €2,243 million and adjusted EBITDA of €362 million. In Q2 2025, revenue was €2,274 million. On a pro forma basis including OPAP, Allwyn's adjusted EBITDA for the 12 months to June 2025 was approximately €1.9 billion. The combined entity's pro forma EBITDA is expected to exceed €2.8 billion, placing it second only to Flutter Entertainment among listed gaming operators globally.

KKCG owns 95.73% of Allwyn, with J&T Arch holding the remaining 4.27%. Post-merger, KKCG will control approximately 85% of total voting rights in the combined company through its ownership of both ordinary and preferred voting shares. Karel Komarek will chair the combined board.

What OPAP Brings

OPAP is Greece's dominant gaming operator, holding exclusive rights to numerical lotteries, land-based sports betting, and video lottery terminals (VLTs) in Greece, and numerical lotteries in Cyprus. It operates an extensive retail network of approximately 3,700 points of sale across Greece and Cyprus, alongside a growing online platform.

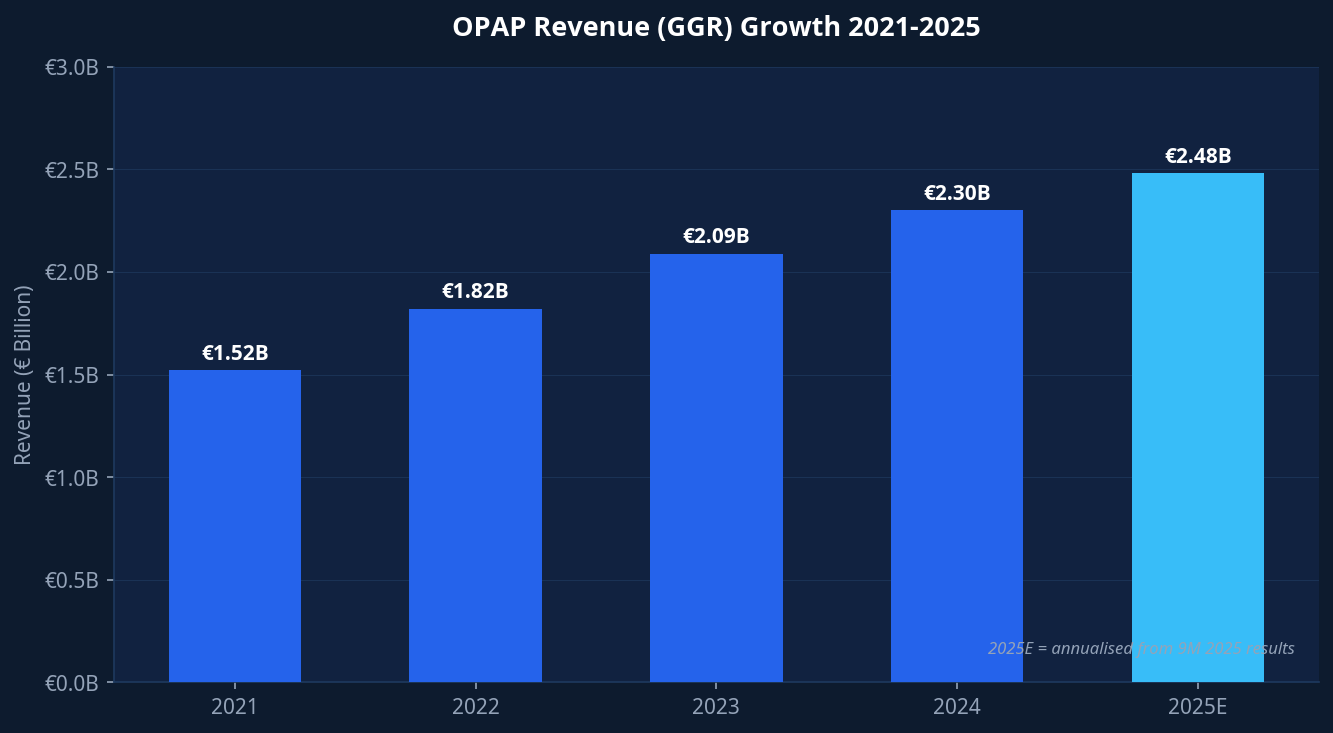

OPAP's financial performance has been consistently strong. GGR (gross gaming revenue) reached €2.3 billion in 2024, up 10% year-on-year from €2.09 billion in 2023. In the first nine months of 2025, GGR was €1,755.9 million, up 6.5% year-on-year, driven by both retail performance and robust online growth. OPAP's quarterly EBITDA has been running at approximately €500-540 million, implying an annualised EBITDA of roughly €900 million on a standalone basis.

OPAP GGR has grown from €1.52B in 2021 to an estimated €2.48B in 2025, a compound annual growth rate of approximately 13%. The 2025 figure is annualised from 9M 2025 results.

OPAP's online channel is the key growth driver. Online GGR has been expanding at a materially faster rate than retail, and the company has invested significantly in its digital platform. The Allwyn combination accelerates this trajectory by deploying Allwyn's proprietary technology stack, which was built to support the UK National Lottery's digital-first operating model, across OPAP's Greek and Cypriot operations.

Transaction Structure

The mechanics of this deal are more complex than a standard acquisition, and understanding the structure is essential to evaluating the economics for each shareholder class.

The transaction proceeds in several steps. First, OPAP hives down its operating business to new Greek subsidiaries and transfers its statutory seat to Luxembourg, creating LuxCo. Second, Allwyn contributes its non-OPAP assets and liabilities to LuxCo in exchange for newly issued shares. Third, the combined company re-domiciles to Switzerland and is renamed Allwyn. Throughout this process, OPAP's listing on the Athens Stock Exchange is maintained, and the combined company remains listed there post-close.

Pre-merger, KKCG controls Allwyn which owns 51.78% of OPAP. Post-merger, KKCG holds approximately 78.5% economic interest and 85% voting rights in the combined entity. OPAP minority shareholders retain 21.5% economic interest.

OPAP minority shareholders (the 48.22% not owned by Allwyn) had two options: accept a cash exit right at a price based on the OPAP closing share price before the transaction, or retain their shares in the combined entity and receive a 21.5% economic interest in the enlarged group. The cash exit window closed on 9 February 2026 with limited take-up, indicating that the majority of minority shareholders elected to remain invested in the combined company. This is a meaningful signal: OPAP's public shareholders broadly endorsed the transaction's long-term value proposition.

Key structural point: The preferred shares issued to Allwyn (€161M, 536.2M shares at €0.30/share) carry a fixed 5% coupon but have no right to ordinary dividends. This creates a two-class economic structure where KKCG captures both the ordinary dividend stream and a fixed preferred return, while OPAP minority shareholders participate only in ordinary dividends. The preferred share mechanism effectively reduces the economic dilution to minority shareholders while giving KKCG additional yield on its contribution.

Strategic Rationale

The stated rationale is scale, technology, and capital markets access. Each deserves scrutiny.

Scale and Market Leadership

The combined entity will be the second-largest listed lottery and gaming operator globally, behind Flutter Entertainment. It will hold market-leading positions in Greece, Cyprus, Czech Republic, Austria, Italy, the UK, and the US (Illinois and Georgia lottery concessions). The geographic diversification reduces dependence on any single regulatory environment and creates a more resilient revenue base. Pro forma EBITDA of approximately €2.8 billion places the combined company in a different tier of the global gaming industry.

Pro forma EBITDA of the combined Allwyn entity versus listed gaming peers. The combination creates the second-largest listed gaming operator by EBITDA, behind Flutter Entertainment.

Technology Deployment

Allwyn has invested heavily in proprietary technology infrastructure, including its Sazka Group platform, which powers lottery operations across multiple markets. Deploying this technology across OPAP's Greek and Cypriot operations is expected to reduce third-party technology costs, accelerate product innovation, and improve the digital customer experience. The UK National Lottery, which Allwyn took over in 2024, provides a live proof of concept for Allwyn's digital-first operating model at scale.

Capital Markets Access

This is arguably the most underappreciated driver. Allwyn has been privately held since its founding. The merger, by maintaining OPAP's Athens Stock Exchange listing and planning an additional listing on London or New York, gives Allwyn access to public equity capital markets for the first time. This is transformative for a company with Allwyn's acquisition appetite. Future bolt-on acquisitions in the lottery and gaming space can be funded with listed equity rather than solely with debt or private capital.

"For investors, this is a unique opportunity to be part of a dynamic company that is shaping the future of entertainment. The combined strength and scale of these multi-billion dollar businesses, massive customer base and Allwyn's continued investment in technology and content, will accelerate innovation and fuel significant international growth."

Karel Komarek, Founder and Chair, Allwyn / KKCG

Geographic Footprint

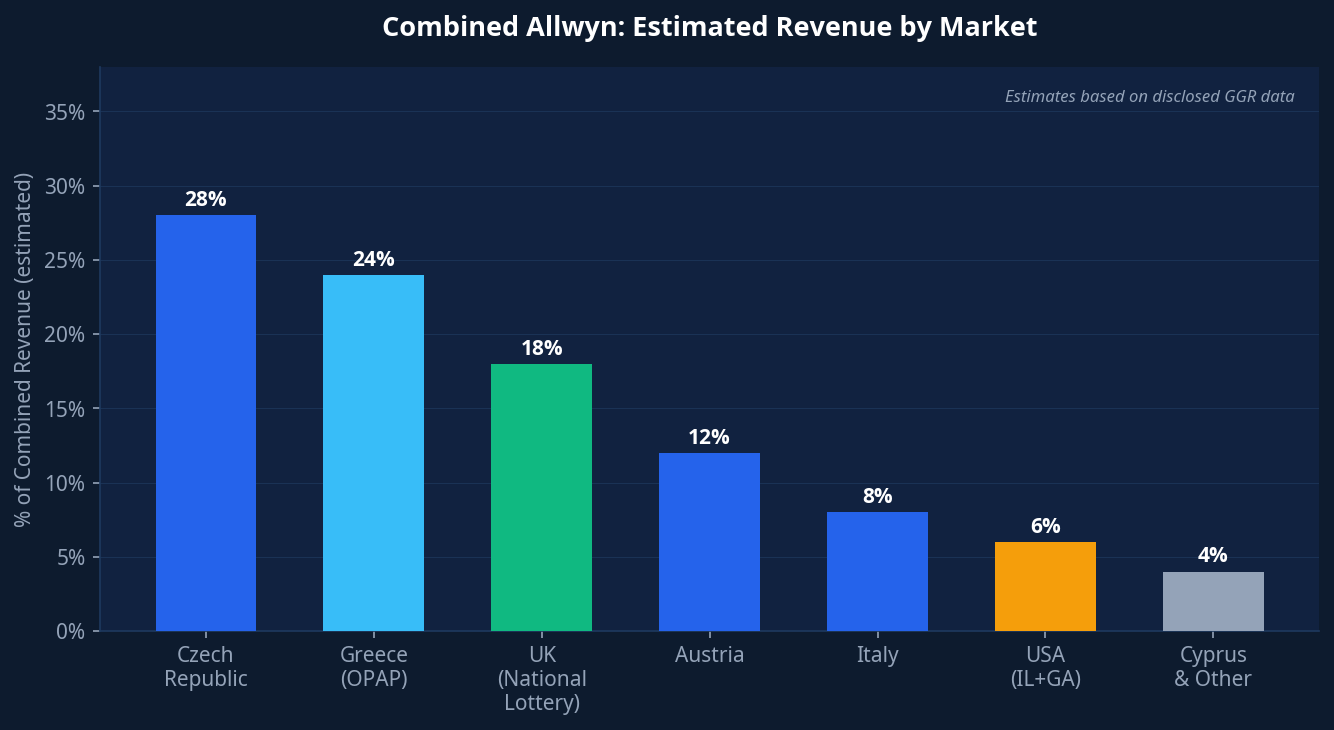

The combined company will operate across 13 markets with a customer base exceeding 50 million. The Czech Republic remains Allwyn's largest single market by revenue, followed by Greece (via OPAP), the UK, and Austria. The US operations, while currently smaller, represent the highest-growth opportunity given the ongoing liberalisation of lottery and gaming markets across American states.

Estimated revenue distribution by market for the combined Allwyn entity. Figures are estimates based on disclosed GGR data from each operating segment. The Czech Republic and Greece together represent approximately 52% of combined revenue.

OPAP's Greek market position is particularly valuable because it is protected by exclusive concession rights. OPAP holds exclusive rights to numerical lotteries and land-based sports betting in Greece through long-term government concessions. The national lottery concession was recently extended to 2037 in exchange for an €80 million upfront fee plus a 30% GGR share. This type of regulatory moat is rare in the global gaming industry and commands a significant valuation premium.

Financial Profile and Capital Allocation

The combined company's financial profile is characterised by high EBITDA margins, strong free cash flow generation, and a moderate leverage position. Net debt to adjusted EBITDA stood at 2.7x on a pro forma basis as of Q2 2025. The medium-term target is approximately 2.5x, with flexibility to exceed this for value-accretive acquisitions with a clear deleveraging path.

| Financial Metric | Allwyn Standalone | OPAP Standalone | Combined (Pro Forma) |

|---|---|---|---|

| Revenue (GGR) | ~€4.5B (annualised) | ~€2.48B (2025E) | ~€7.0B+ |

| Adjusted EBITDA | ~€1.9B (LTM Jun 2025) | ~€900M (est.) | ~€2.8B+ |

| Net Debt / EBITDA | 2.7x (Q2 2025 pro forma) | Target ~2.5x | |

| Minimum Dividend | €1.00/share from FY2026 | ||

| Post-Close Dividend | €0.80/share (in lieu of 2025 remainder) | ||

| EPS Accretion | Double-digit in first full year post-close | ||

The dividend policy is a key feature of the investment case. OPAP has historically been a high-dividend payer, and the combined company commits to a minimum annual dividend of €1.00 per share from FY2026, with a scrip option available. Special dividends and buybacks are also contemplated. For OPAP's existing minority shareholders, this represents continuity of the income stream they have historically valued.

Regulatory Pathway

The transaction requires approval from the Hellenic Gaming Commission (HGC) in Greece, alongside other customary regulatory approvals across Allwyn's operating jurisdictions. The HGC approval is the primary gating item. Given that Allwyn already owns 51.78% of OPAP and has been its controlling shareholder since 2013, the regulatory relationship is well-established. The HGC is not evaluating a new entrant; it is reviewing a consolidation of existing ownership.

S&P Global revised Allwyn's outlook to Stable in February 2026, noting an elevated likelihood that the transaction will close by the end of H1 2026. S&P is already fully consolidating OPAP in Allwyn's credit metrics, which is a strong signal that the rating agency views the regulatory risk as manageable.

Regulatory risk flag: The Hellenic Gaming Commission approval is the primary outstanding condition. While the relationship between Allwyn and the Greek regulatory environment is long-standing, any change in Greek government policy toward gaming, or any adverse finding during the HGC review process, could delay or complicate the close. The transaction is also subject to approvals in other jurisdictions where Allwyn operates, though these are considered lower risk.

Valuation Analysis

The €16 billion equity value implies a combined EV/EBITDA multiple of approximately 5.7x on pro forma EBITDA of €2.8 billion, assuming net debt of approximately €2.5 billion (2.7x EBITDA). This is a modest multiple for a business with the combined entity's market positions, cash flow characteristics, and growth profile.

| Comparable | EV/EBITDA | Revenue Multiple | Notes |

|---|---|---|---|

| Flutter Entertainment | ~14x | ~3.5x | Largest listed gaming operator; FanDuel premium |

| Entain | ~8x | ~2.0x | UK-listed; sports betting and gaming |

| IGT | ~7x | ~2.5x | Lottery technology and operations |

| Scientific Games | ~9x | ~3.0x | Lottery systems and instant games |

| Combined Allwyn (implied) | ~5.7x | ~2.3x | Significant discount to peers |

The implied discount to peers reflects several factors: the Athens Stock Exchange listing (which attracts a lower valuation multiple than London or New York), the complexity of the transaction structure, and the fact that Allwyn has not previously been publicly traded and therefore lacks an established analyst coverage base. The planned secondary listing on London or New York is explicitly designed to close this valuation gap over time.

From OPAP minority shareholders' perspective, the transaction is accretive. The combined company is projected to deliver double-digit EPS accretion in the first full year post-completion, normalised for the temporary benefit of the GGR contribution prepayment. The minimum €1.00/share dividend commitment provides income floor visibility.

Key Risks

| Risk | Severity | Assessment |

|---|---|---|

| Hellenic Gaming Commission delay | Medium | Primary gating item. Long-standing relationship reduces risk but cannot be eliminated. |

| Greek regulatory / political risk | Medium | OPAP's concession rights are government-granted. Any shift in Greek gaming policy affects the core asset. |

| Integration complexity | Medium | Merging 13-market operations across multiple regulatory regimes, languages, and technology stacks is operationally demanding. |

| UK National Lottery execution | Medium | Allwyn took over the UK National Lottery in 2024. Any operational issues in the UK could distract management and affect the combined company's credibility. |

| Leverage | Low-Medium | 2.7x net debt/EBITDA is manageable for a cash-generative business. Rising interest rates could increase cost of debt on refinancing. |

| Athens Stock Exchange valuation discount | Medium | The primary listing in Athens limits institutional investor access. The secondary listing plan is the mitigation, but timing is uncertain. |

| KKCG concentration risk | High | KKCG controls 85% of voting rights post-merger. Minority shareholders have limited ability to influence governance outcomes. |

Scenario Analysis

€20B+ Equity Value by 2028

HGC approval in Q2 2026, secondary listing on London Stock Exchange by end of 2026, re-rating to 7-8x EBITDA as institutional coverage builds. US lottery operations expand to additional states. Online GGR in Greece grows 25%+ annually.

€16-18B Equity Value, Stable Dividends

Close in H1 2026 as planned. Secondary listing delayed to 2027. Valuation re-rates modestly to 6-6.5x EBITDA as combined entity delivers on EBITDA accretion and dividend commitments. Steady state cash generation supports €1.00+ annual dividend.

Close Delayed to H2 2026 or 2027

HGC approval delayed by regulatory process or political intervention. Secondary listing postponed. OPAP minority shareholders face extended uncertainty. UK National Lottery operational issues distract management. Valuation discount persists.

Acquiry View

This transaction is structurally sound and commercially logical. Allwyn has been building toward this consolidation since KKCG first invested in OPAP in 2013. The 12-year relationship between the two entities means the integration risk is lower than it would be for a true third-party acquisition. The technology deployment thesis is credible: Allwyn's platform has been proven across multiple markets, and OPAP's Greek operations are a natural next deployment target.

The valuation mechanics are interesting. The €16 billion equity value looks conservative relative to listed gaming peers, but this reflects the Athens Stock Exchange discount and the complexity premium of a multi-step cross-border transaction. The planned secondary listing is the key value unlock. If Allwyn achieves a London or New York listing within 12-18 months of closing, and the combined entity delivers on its EBITDA accretion targets, a re-rating toward 7-8x EBITDA is achievable, implying an equity value of €18-20 billion.

The governance structure is the primary concern for minority shareholders. KKCG's 85% voting control means that all material decisions, including future acquisitions, capital allocation, and dividend policy, are effectively controlled by Karel Komarek. The two independent non-executive directors on the eight-person board provide limited protection. Investors taking a position in the combined entity are making a bet on Komarek's judgment and execution capability, not on a governance structure that provides meaningful minority protection.

For M&A practitioners, this deal is a useful case study in how a private company can achieve a public listing through a reverse merger with a controlled subsidiary, while simultaneously consolidating ownership and accessing equity capital markets. The structure is replicable in other markets where a controlling shareholder holds a majority stake in a listed entity and wishes to bring private assets into the public vehicle.

Acquiry transaction note: The gaming and lottery sector is entering a consolidation phase driven by regulatory moat scarcity, technology investment requirements, and the need for scale to compete in digital channels. Allwyn's strategy of acquiring exclusive concession rights across multiple jurisdictions and deploying a unified technology platform is the dominant playbook in this sector. Operators without comparable scale or technology will face increasing pressure to sell or merge over the next five years.